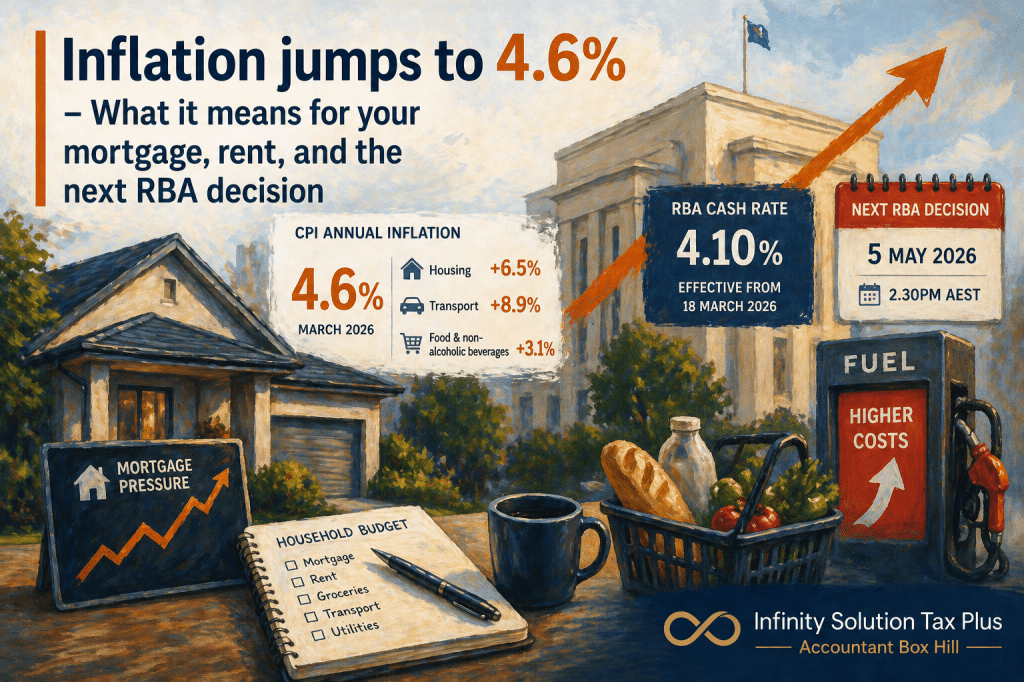

Australia’s inflation picture worsened on 29 April 2026, with the ABS reporting that annual CPI rose to 4.6% in March, up from 3.7% in February. The largest contributors were Housing (+6.5%), Transport (+8.9%), and Food and non-alcoholic beverages (+3.1%). For households, that means cost-of-living pressure is no longer just a headline story — it is showing up directly in mortgage stress, rent negotiations, and everyday spending.

For anyone speaking with an accountant Box Hill, the immediate question is not just whether prices are rising, but what this means for the next Reserve Bank move and for household cash flow over the next few months. The RBA’s cash rate target is currently 4.10%, effective from 18 March 2026, and the next monetary policy update is scheduled for 5 May 2026 at 2.30 pm AEST.

Why the March inflation result matters

A 4.6% annual CPI reading is well above the RBA’s 2–3% inflation target band. However, the March data also showed trimmed mean inflation at 3.3%, unchanged from February. That matters because the RBA pays close attention to underlying inflation measures when volatile items such as fuel move sharply. The Bank explains that trimmed mean inflation removes the largest price changes and gives a better read on broad inflation pressure across the economy.

In practical terms, this means the RBA is likely to view March as a serious inflation setback, but not necessarily in the same way as if underlying inflation had also surged sharply. The jump is largely due to a fuel shock, with petrol prices flowing through to transport costs and broader household budgets.

What it means for mortgage holders

Mortgage borrowers should prepare for the real possibility that the RBA keeps rates higher for longer, even if it does not raise them immediately on 5 May. The cash rate has a strong influence on lending rates, and the RBA notes that monetary policy decisions affect mortgage rates, deposit rates, economic activity, and inflation across the economy. For variable-rate borrowers, that means repayments may stay elevated for longer than many households were hoping.

What it means for renters

Renters are also exposed, even without a mortgage. Housing was one of the largest contributors to annual inflation, and higher borrowing costs can continue to pressure landlords’ financing costs and investment decisions. While rent movements vary by suburb and vacancy conditions, a sticky housing inflation number usually means rental affordability remains under strain.

What should households do?

The best response is not panic, but a reset of the household budget. MoneySmart recommends starting with a written budget, using a budget planner, reviewing recurring bills, and tracking spending before costs drift further. Their cost-of-living guidance also highlights mortgage interest, groceries, and petrol as key pressure points worth reviewing first.

For many families, this is the moment to revisit fixed versus variable loan settings, emergency savings buffers, and how much room there is in the budget if rates stay high through winter. A Box Hill accountant can also help households and small business owners understand the broader cash-flow effect where personal and business finances overlap.

Final thoughts

The March 2026 CPI result is a reminder that inflation shocks can return quickly, even after earlier signs of moderation. The next RBA decision on 5 May 2026 now carries extra weight, but the bigger issue for households may be the prospect of rates staying restrictive for longer rather than one single meeting outcome. Early budgeting, realistic repayment planning, and informed advice from a trusted accountant in Box Hill can make that pressure more manageable.

Disclaimer: This article contains general information only and does not constitute financial or taxation advice. You should seek personalised advice from a registered tax or financial professional.