The Reserve Bank increased the cash rate to 3.85% in February 2026, citing inflation risks that remain under close watch. With households already feeling higher borrowing costs, recent reporting has highlighted renewed anxiety about further rate rises — including commentary about a possible move to 4.1%.

No one can predict the exact path of interest rates. But borrowers can control how prepared they are. If the cash rate were to move to 4.1% or higher, variable mortgage holders would typically face higher repayments — though the impact depends on how their lender passes changes through.

For many households speaking with an experienced accountant Box Hill, the key is preparation — not panic.

Step 1: Understand the Current Rate Environment

The RBA’s February statement confirmed the 3.85% cash rate and made clear inflation remains a key risk to monitor. Inflation data continues to shape these decisions — the ABS reported CPI rose 3.8% over the year to January 2026.

When inflation remains above target:

- Borrowing costs can stay elevated

- Lenders may adjust variable rates (often quickly)

- Household cash flow tightens

Global oil and energy price volatility can also influence inflation expectations and add uncertainty.

Important note: the cash rate is not your mortgage rate. Your repayment changes depend on your lender rate, your remaining term, and whether you’re fixed, variable, or split.

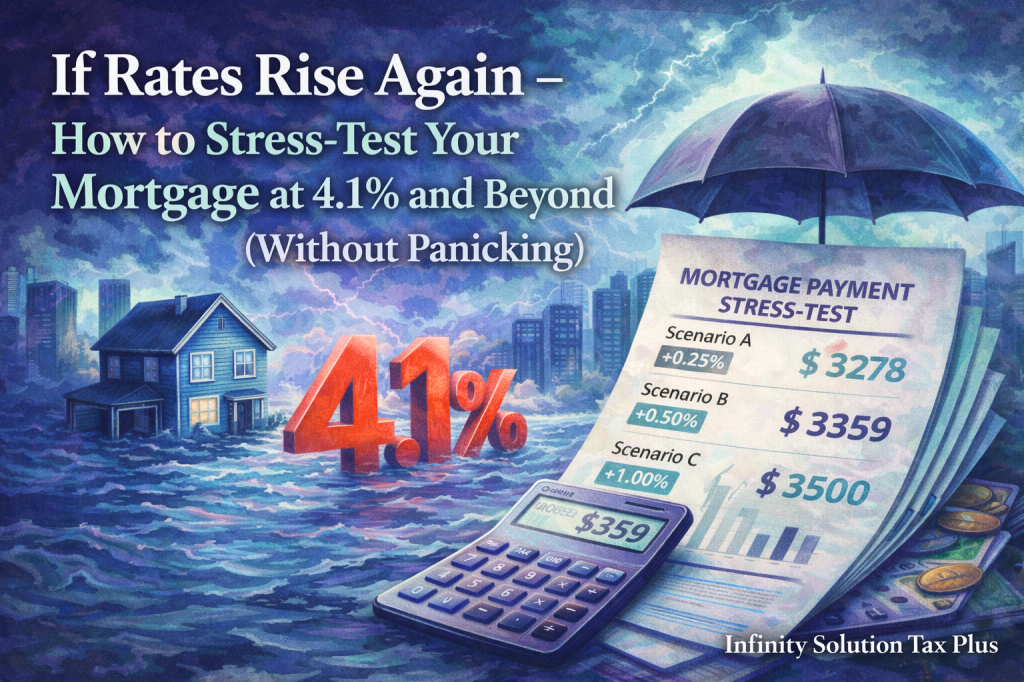

Step 2: Stress-Test at 4.1% (or Higher)

A practical stress test isn’t about predicting the RBA. It’s about building a buffer against “what if” scenarios.

Run two simple scenarios:

- Scenario A: Your current mortgage rate + 0.25%

- Scenario B: Your current mortgage rate + 0.50% (or even +1.00% if you want a tougher test)

Then:

- Recalculate monthly repayments under each scenario

- Compare the increase to your monthly surplus

- Ask: Can we absorb this without using credit?

For example:

- On a $600,000 loan, a 0.25% rate rise adds meaningful interest over a year (the exact dollar impact depends on your rate and remaining term).

- A 0.50% rise increases that impact further.

The key question: If repayments rise, what specific line item changes first — and by how much?

A qualified accountant in Box Hill can also help assess after-tax cash flow, especially if the property is an investment where interest is generally deductible (subject to your circumstances and current tax law).

Step 3: Identify Adjustment Levers Early

If your stress test shows pressure, the goal is to increase flexibility before you’re forced to act.

Potential adjustments include:

- Redirecting surplus into an offset account (if available)

- Reviewing discretionary spending (subscriptions, dining out, impulse shopping)

- Negotiating with your lender on rate discounts or features

- Reviewing fixed vs variable split (noting break costs and flexibility)

- Extending loan terms with caution (lower repayments now can mean more interest over time)

The objective is not drastic lifestyle cuts. It’s creating room to move.

Step 4: Build a 2-3 Month Buffer

In uncertain cycles, liquidity often matters more than “perfect optimisation”.

Aim to build:

- Two to three months of mortgage repayments, plus

- Essential living expenses (utilities, groceries, insurance)

This buffer reduces emotional decision-making if rates rise again or income fluctuates.

If building three months feels too big, start with two smaller targets:

- $1,000 buffer, then two months of repayments, then three months.

Step 5: Consider the Tax and Structure Impact

For owner-occupiers, interest is generally not tax-deductible. For investors, interest is typically deductible (depending on how the loan is used), which changes the effective after-tax cost of a rate rise.

Understanding:

- Your marginal tax rate

- Whether interest is deductible in your situation

- After-tax cash flow (not just the repayment amount)

can significantly change how a rate move “feels” financially.

Strategic planning with a trusted accountant in Box Hill helps ensure mortgage decisions align with your broader tax position — and that you don’t accidentally weaken deductibility or cash flow through rushed restructuring.

Avoid Panic Reactions

When headlines focus on rate fears, households often:

- Make rushed refinancing decisions without comparing total costs

- Overextend into risky short-term credit

- Liquidate long-term investments prematurely

Rate cycles respond to inflation data and economic conditions. Prepared borrowers keep options open, rather than locking in decisions under stress.

Final Thoughts

With the cash rate currently at 3.85%, a move to 4.1% or beyond is a scenario worth modelling — not fearing.

Stress-testing your mortgage now provides clarity. It lets you identify manageable adjustments, build buffers, and reduce uncertainty before it becomes urgent.

In a higher-rate environment, informed planning is more valuable than prediction.

Disclaimer: This article contains general information only and does not constitute financial or taxation advice. You should seek personalised advice from a registered tax or financial professional.