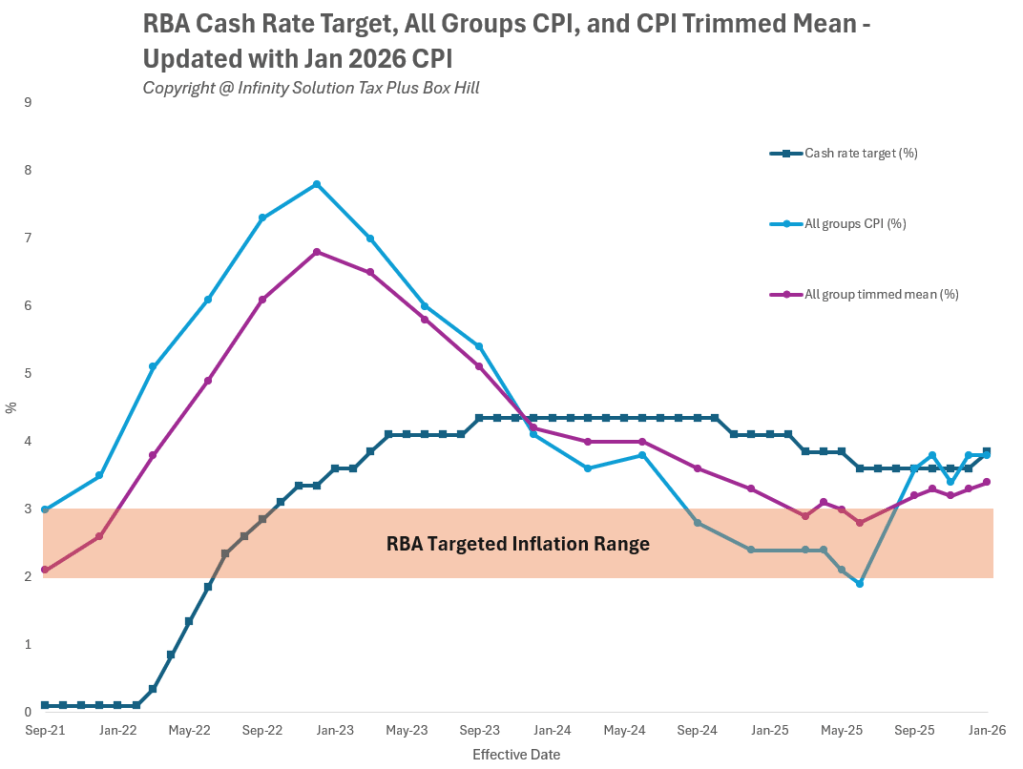

The Reserve Bank of Australia (RBA) has indicated that a March interest rate increase is a “live” possibility, with Governor Michele Bullock noting in recent commentary that renewed inflation risks — including volatility in global oil prices — remain a factor in the Board’s considerations.

This shift in tone follows the RBA’s February monetary policy decision, where the Board outlined its updated assessment of inflation, economic growth, and labour market conditions. While no decision has yet been made, some economists suggest a further rise remains possible depending on upcoming inflation data and global developments.

For households and investors, the key question is not whether rates might rise — but what a move would mean in practical terms. For many clients speaking with an accountant Box Hill, the focus is on cash flow, debt management, and forward planning.

Why the RBA Is Concerned Again

Oil Prices and Inflation Risk

The RBA has highlighted global energy price volatility as a potential driver of renewed inflation pressure.

Higher oil prices can affect inflation through:

- Increased fuel and transport costs

- Higher business operating expenses

- Flow-on effects to consumer goods and services

If businesses pass these costs on, headline inflation may remain elevated for longer than forecast. The Australian Bureau of Statistics (ABS) details how fuel and transport costs feed into CPI calculations.

What a Rate Rise Means for Borrowers

Variable Mortgage Holders

If banks pass on a 0.25% increase in full (assuming a standard 25–30 year principal and interest loan):

- A $600,000 mortgage could rise by roughly $125 per month.

- A $900,000 mortgage could increase by $190 per month.

Actual repayment changes will vary depending on loan term, interest rate, and structure.

For property investors, this directly affects:

- Net rental yield

- Serviceability

- Negative gearing cash flow assumptions

A proactive discussion with a Box Hill accountant can help stress-test repayment capacity under different rate paths.

What About Rents?

Landlords facing higher interest costs may attempt to lift rents at renewal. However, rental increases are ultimately constrained by:

- Tenant affordability

- Local vacancy rates

- State-based tenancy laws

In tighter rental markets, upward pressure is more likely. In more balanced or oversupplied areas, landlords may need to absorb higher holding costs instead.

The Quiet Winner: Savers

While borrowers feel the impact first, savers may benefit.

Higher cash rates typically:

- Lift term deposit rates

- Improve returns on high-interest savings accounts

- Increase income for retirees relying on interest earnings

However, banks do not always pass on rate increases evenly between borrowers and depositors, as pricing decisions also reflect funding costs and competitive pressures.

Planning Considerations

Households should consider:

- Reviewing variable vs fixed loan splits

- Building repayment buffers

- Reassessing discretionary spending

- Reviewing investment debt structures

- Considering the tax implications of higher deductible interest (for investors)

Interest on investment loans generally remains tax-deductible where funds are used for income-producing purposes, subject to ATO requirements and proper loan tracing. However, rising rates as well as the possible tax reform to CGT and negative gearing can still strain both short-term and long-term cash flow.

Infinity Solution Tax Plus, as a trusted accountant in Box Hill, works with individuals and investors to assess debt structures, tax positioning, and long-term sustainability rather than reacting to headlines.

Final Thoughts

The RBA has not yet moved — but describing a March hike as “live” indicates the Board considers multiple outcomes possible.

Upcoming inflation data, labour market conditions, and global energy developments will likely shape the final decision. For households, early planning is generally more effective than last-minute adjustments.

Understanding how even small rate changes affect repayments, rents, and savings is increasingly important in a higher-rate environment.

Disclaimer: This article contains general information only and does not constitute financial or taxation advice. You should seek personalised advice from a registered tax or financial professional.