A proposal gaining attention this week suggests introducing HECS-style loans to help retirees fund home electrification upgrades — such as solar panels, batteries, or efficient appliances — with repayments structured similarly to income-contingent student loans.

The debate comes as households face renewed pressure on energy bills, following confirmation that broad-based federal energy bill relief would not be extended beyond its current settings.

For homeowners — particularly retirees on fixed incomes — the question is practical: do the long-term savings justify the upfront cost and repayment structure? As any experienced accountant Box Hill would advise, the answer depends on cash flow, time horizon, and risk tolerance.

Why Electrification Is Being Discussed Now

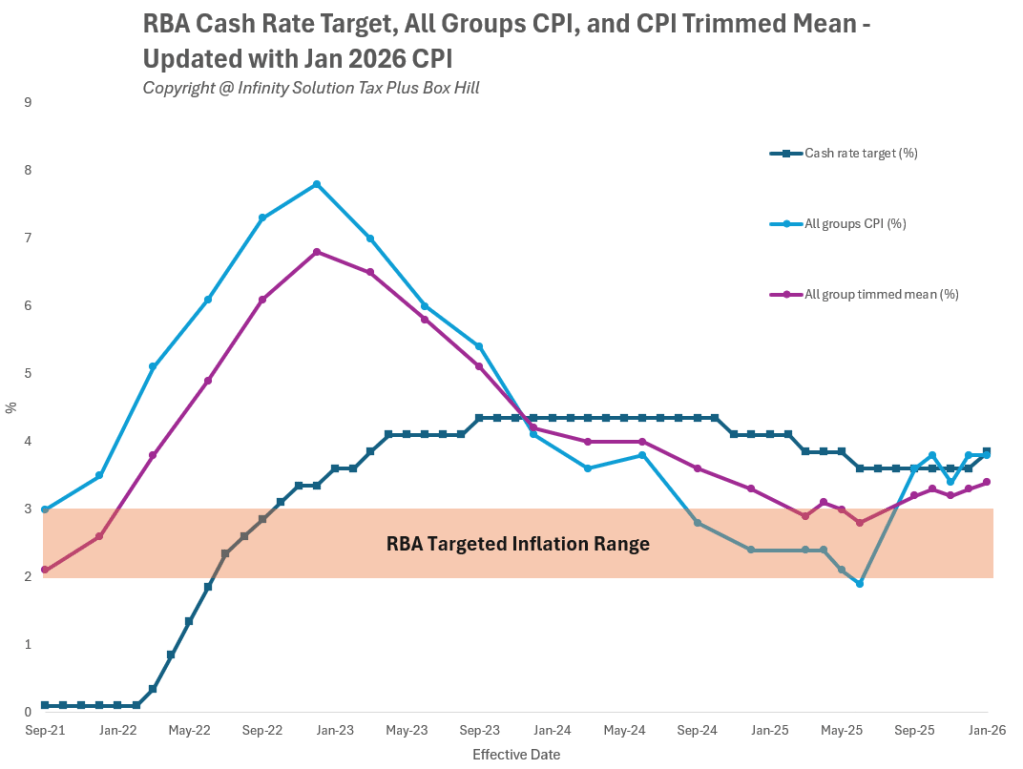

Energy costs have contributed to household budget pressures and broader inflation dynamics, with CPI rising 3.8% over the year to January 2026.

While government rebates have provided temporary relief, long-term structural bill reductions typically require capital investment in:

- Rooftop solar systems

- Home batteries

- Electric heat pumps

- Induction cooktops

- Improved insulation

The 2025–26 Federal Budget included targeted cost-of-living measures, but energy bill relief measures were not designed as permanent subsidies.

This policy backdrop has prompted discussion about alternative financing mechanisms to make upgrades more accessible.

How a HECS-Style Model Would Work

Although details remain proposal-based rather than legislated policy, a HECS-style structure generally implies:

- No large upfront payment

- Repayments linked to income

- Possible deferral below income thresholds

- Government-backed financing

The appeal for retirees is clear: reduced immediate financial strain while benefiting from lower electricity bills.

However, financing costs still matter. Traditional HECS/HELP loans are indexed to inflation rather than charging commercial interest, and similar indexation features have been suggested in public discussion. Broader borrowing conditions across the economy are influenced by the Reserve Bank’s cash rate.

Even income-contingent loans may carry indexation adjustments, meaning total repayment amounts can increase over time.

Are the Savings Realistic?

Electrification can deliver genuine long-term savings — but outcomes vary significantly based on:

- Household energy usage

- Solar generation capacity

- Tariff structures

- Battery payback periods

- Property suitability

Savings projections cited in media reporting can be scenario-based and depend heavily on assumptions about future electricity prices, export feed-in tariffs, and system performance.

For retirees planning to remain in their homes long term, a 7–10 year payback period may be reasonable under certain conditions. For those considering downsizing within a few years, the economics may be less compelling unless resale value uplift offsets installation costs.

Who Should Consider It Carefully?

Retirees on fixed incomes: Income-linked repayments may provide flexibility, but total lifetime repayment cost should be modelled conservatively.

Homeowners nearing sale: Property value uplift should be assessed realistically rather than assumed.

Self-funded retirees: Financing arrangements may affect broader asset structuring decisions and cash flow planning.

A detailed financial review with a qualified Box Hill accountant can help evaluate repayment modelling, tax implications, and long-term affordability.

Final Thoughts: Policy Innovation, But Do the Numbers

HECS-style electrification loans aim to combine cost-of-living support with long-term energy transition goals. For some households, they may provide structured access to upgrades without upfront capital strain.

However, no financing model removes the need for careful analysis. Savings projections should be conservative, repayment assumptions realistic, and personal circumstances central to the decision.

At Infinity Solution Tax Plus, a trusted accountant in Box Hill can assist retirees and homeowners in assessing whether energy upgrades align with their broader financial strategy — ensuring decisions are driven by long-term sustainability rather than short-term headlines.

Disclaimer: This article contains general information only and does not constitute financial or taxation advice. You should seek personalised advice from a registered tax or financial professional.