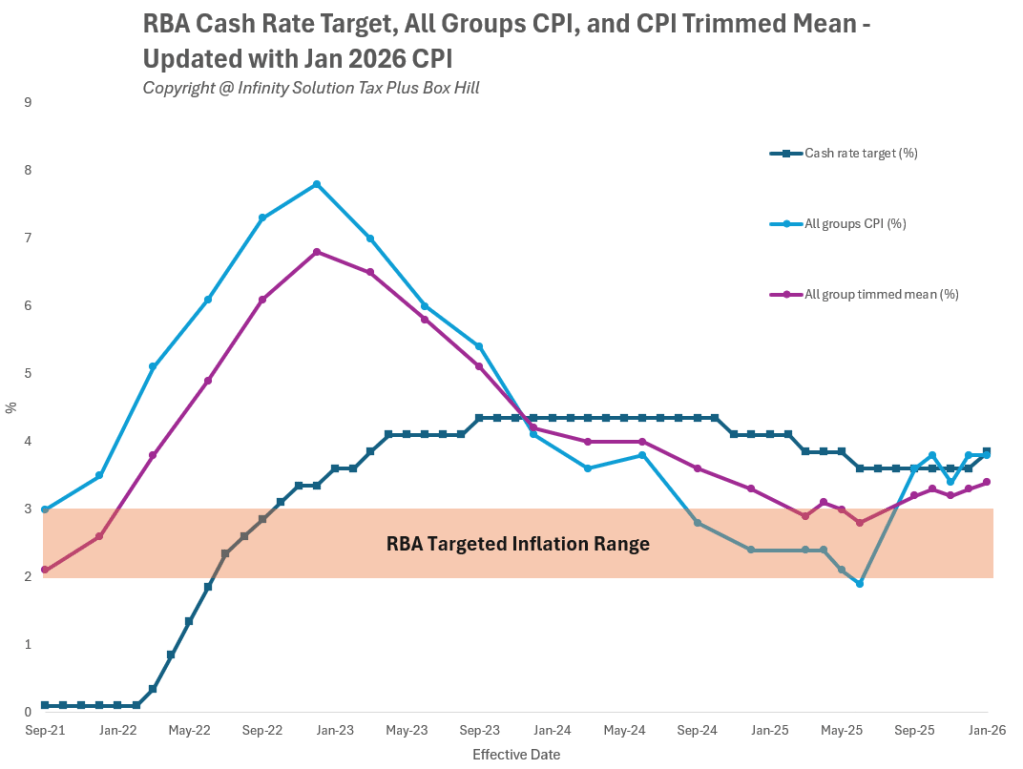

With recent rate increases influencing borrowing capacity and buyer confidence, many households are feeling the pressure through higher mortgage repayments. Behind the headlines, the mechanism is straightforward: when the Reserve Bank of Australia (RBA) adjusts the cash rate, lenders commonly adjust mortgage rates. As at 4 February 2026, the cash rate target is 3.85%. For many borrowers, that translates into higher monthly repayments — and the need for a structured budget reset.

As an accountant Box Hill households consult when financial conditions tighten, we recommend a practical, measured review rather than reactive decision-making.

Step 1: Recalculate Your True Repayment Position

Start with the updated repayment figure from your lender and calculate:

- Your new minimum monthly repayment

- The total annual increase in repayments

- Your remaining buffer after essential expenses

Even a 0.25% rate rise can meaningfully affect annual cash flow on a large mortgage.

At the same time, broader cost-of-living pressures remain relevant. The ABS Selected Living Cost Indexes show changes in living costs across household types in the year to the December 2025 quarter, highlighting how mortgage increases can coincide with broader expense pressures.

When rising repayments combine with higher everyday costs, budget stress can compound quickly.

Step 2: Separate Fixed, Variable and Discretionary Spending

A simple three-category structure helps clarify where adjustments are possible:

Fixed commitments

- Mortgage

- Utilities

- Insurance

- School fees

Variable essentials

- Groceries

- Fuel

- Transport

Discretionary

- Dining out

- Subscriptions

- Travel

If repayments have risen, prioritise adjusting discretionary spending first before reducing essential protections such as insurance coverage.

Step 3: Review Loan Structure

Consider discussing with your lender or broker:

- Whether your interest rate remains competitive

- The suitability of partial fixed vs variable splits

- Effective use of offset accounts

- Whether loan term adjustments would assist cash flow

A Box Hill accountant can assist with modelling the cash-flow and tax implications of refinancing decisions (particularly where investment properties are involved), while licensed credit advisers provide regulated loan product advice.

Step 4: Protect Yourself From Scams During Financial Reviews

Periods of financial stress often coincide with increased scam activity. The ATO publishes scam alerts warning Australians about fraudulent messages impersonating government agencies. If you receive suspicious communication related to tax, superannuation, refinancing, or government payments, you can verify or report it directly through official ATO channels.

When reviewing finances online, access accounts directly via official websites rather than clicking unknown links in emails or messages.

Step 5: Seek Early Support If Stress Is Building

Mortgage stress rarely begins at default — it usually begins when:

- Savings buffers are shrinking

- Credit card balances are rising

- Short-term debt is being used to meet repayments

Early discussions with your lender may open access to hardship arrangements or temporary repayment adjustments. Financial counsellors can also provide free, confidential assistance.

Who Is Most Vulnerable?

Borrowers typically more exposed to rate movements include:

- Recent purchasers with high loan-to-value ratios

- Households rolling off previously fixed low-rate loans

- Single-income households

- Investors with multiple leveraged properties

In these cases, proactive cash-flow modelling becomes particularly important.

Final Thoughts

Rate cycles are part of Australia’s economic landscape — but their impact on household budgets is immediate. A structured budget reset, early review of loan terms, and disciplined expense management can prevent short-term pressure from becoming long-term financial strain.

At Infinity Solution Tax Plus, a trusted accountant in Box Hill, we assist clients in reviewing cash-flow positions, modelling repayment scenarios, and aligning property decisions with broader tax and financial strategies.

A calm, early reset is often the most effective response to a rising-rate environment.

Disclaimer: This article contains general information only and does not constitute financial or taxation advice. You should seek personalised advice from a registered tax or financial professional.