Sydney’s auction market is showing the early behavioural effects of higher interest rates: a larger share of properties selling before auction, fewer auctions scheduled, and buyers negotiating harder as borrowing costs rise. Recent reporting noted an increase in pre-auction transactions (around 24% in parts of Sydney) alongside a softer auction run-rate compared with the same period last year.

For households, this is less about headlines and more about what higher repayments do to budgets, borrowing capacity, and sale timelines. As an accountant Box Hill clients often speak with when plans involve property, debt, and cash-flow, we’re seeing more people reassess their “next step” before they commit to a purchase, a sale, or a refinance.

The key is understanding what has changed — and what you can control.

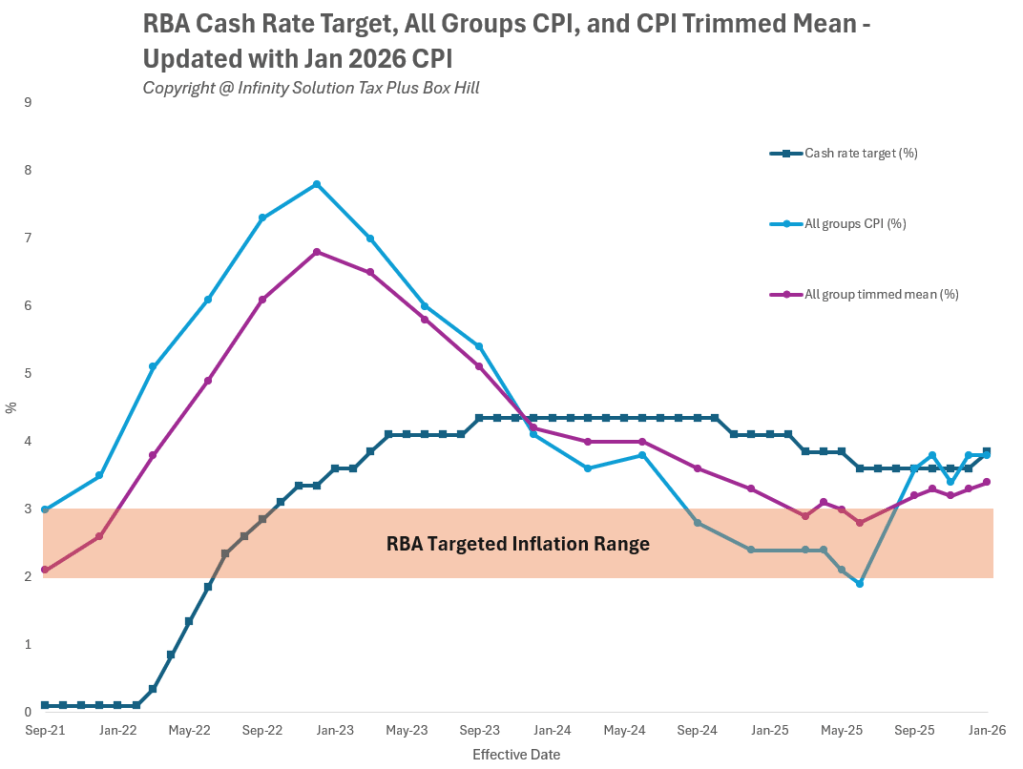

What the RBA Cash Rate Move Really Does

The Reserve Bank of Australia (RBA) sets a cash rate target that influences interest rates across the economy, including mortgage and deposit rates. As of 4 February 2026, the cash rate target is 3.85%, and the RBA lists its next scheduled update for 17 March 2026

In its February 2026 communications, the RBA stated it lifted the cash rate target by 25 basis points to 3.85% in response to inflation conditions and its broader objectives of price stability and full employment.

In practical terms, when the cash rate rises, lenders commonly reprice variable home loans (and may also adjust fixed-rate pricing depending on wholesale funding costs). For borrowers, this usually means higher minimum repayments and/or reduced maximum borrowing capacity under lender serviceability tests.

Buyers: Borrowing Capacity, Bidding Psychology, and Timing

In higher-rate conditions, buyers typically feel the change in three places:

- Serviceability and borrowing capacity (what the bank will lend)

- Monthly repayments (what the loan costs)

- Confidence at auction (how hard buyers bid when finance is tighter)

This helps explain why more transactions can shift to pre-auction offers: it can give buyers more control (often “subject to finance”) and give sellers more certainty without relying on auction-day momentum.

A practical planning move is to re-check your numbers before you start offering — especially if your pre-approval was assessed under a lower-rate setting, or if your lender’s servicing assumptions have changed since you applied.

Sellers: Reserve Prices, “Days on Market”, and Negotiation Power

For sellers, higher rates can shift the balance from “auction theatre” to “best-offer pragmatism”. When borrowing capacity tightens, buyer depth can thin in certain price brackets, and vendors often respond with:

- more realistic reserves

- greater openness to pre-auction or prior-to-auction negotiations

- tighter focus on presentation to reduce “discounting” pressure and buyer objections

If you’re selling and buying in the same cycle, remember that rate changes can affect both sides — your sale outcome and your next borrowing capacity — so planning the sequence and settlement timing matters.

Refinancers: A Cash-Flow Check-Up Worth Doing

Even when rates are higher overall, refinancing can still be worthwhile if it improves net cash flow (after fees) or reduces risk (for example, fixing part of the loan to reduce repayment volatility).

A Box Hill accountant can help you map the tax and cash-flow side of the decision (especially where investment property is involved), but loan product advice should come from a licensed credit professional.

Cost-of-Living Pressure Is Part of the Story

Rate rises land differently depending on household type and spending mix. The ABS Living Cost Indexes showed annual living-cost increases across household types in the 12 months to the December 2025 quarter, underscoring why a realistic repayment buffer matters when mortgage costs rise.

Final Thoughts

Higher rates don’t stop property markets — they change how decisions get made. Expect more negotiation, more sensitivity to finance clauses, and more scrutiny on repayment comfort.

If you’re planning a move in 2026, bring forward the “numbers check” so you can act decisively when the right opportunity appears. Infinity Solution Tax Plus, a trusted accountant in Box Hill, can help you understand the tax and cash-flow implications around property decisions and refinancing discussions, and coordinate with your broker or adviser where required.

Disclaimer: This article contains general information only and does not constitute financial or taxation advice. You should seek personalised advice from a registered tax or financial professional.