The Federal Government’s push to reshape superannuation tax concessions has returned to the spotlight, with renewed focus on Division 296 and broader “better targeted superannuation concessions” reforms. Recent reporting has discussed higher effective tax rates on very large super balances, including commentary about potential future tiers in wider “wealth tax” debates.

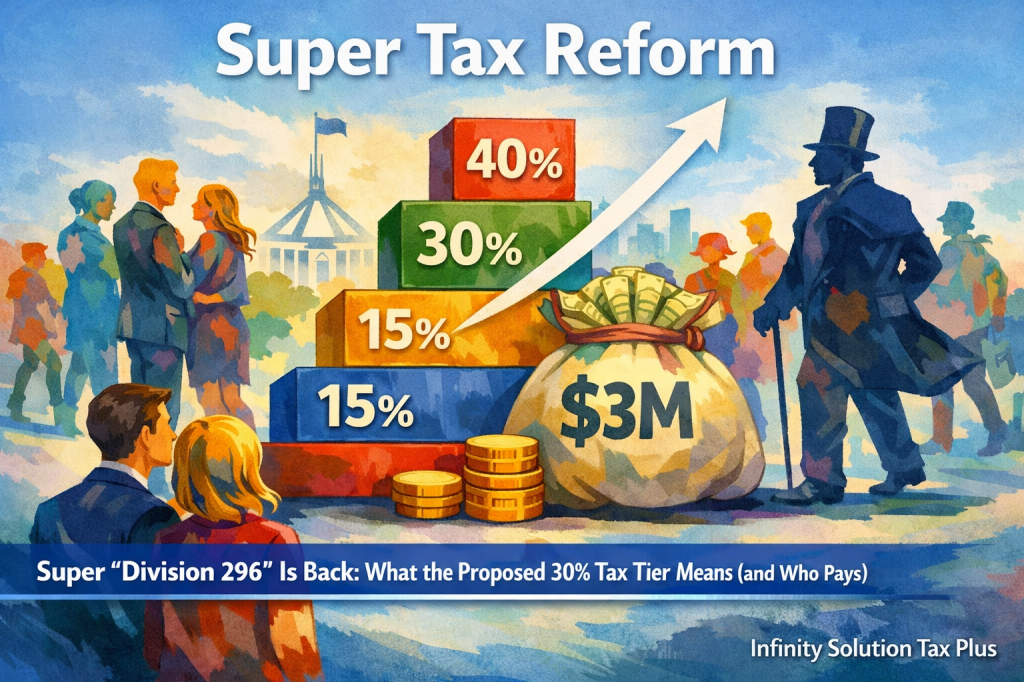

Importantly, under the current legislative design, Division 296 introduces an additional 15% tax on certain earnings linked to super balances between $3 million and 10 million – effectively increasing the tax rate on that portion from 15% to 30%. For super balances above $10 million, up to an overall 40% tax rate will be applied.

At the core of the measure is the Government’s stated objective to make super concessions “more sustainable and better targeted”, particularly at very high balances. The ATO has outlined how the proposed Division 296 framework is intended to operate and who it captures.

For individuals reviewing their retirement strategy with an experienced accountant Box Hill, this is no longer an abstract policy debate — it is forward planning.

What Is Division 296?

Division 296 introduces an additional tax on earnings attributable to superannuation balances above $3 million.

Under the design outlined by Treasury and the ATO:

- The measure applies to individuals (not funds directly).

- It targets the proportion of earnings linked to balances exceeding $3 million.

- The additional tax rate is 15% on that proportion of earnings (effectively lifting the rate from 15% to 30% on those earnings).

- It is calculated annually based on total super balance movements.

How Is the Tax Calculated?

A key feature — and source of concern — is that the calculation is based on changes in total super balance, not just realised income.

This means:

- Growth in asset values may be included in the earnings calculation.

- The tax liability arises even if assets are not sold.

- Individuals can choose to pay the liability personally or release funds from super.

Professional commentary from the SMSF sector highlights liquidity and valuation considerations, particularly for trustees holding property or illiquid assets.

The good news is, for many Australians, the $3 million threshold is well above typical retirement balances, with less than 0.5% Australians will be affected by this change.

Who Is Affected?

The policy primarily impacts:

- Individuals with total super balances exceeding $3 million.

- SMSF members with concentrated property or private asset holdings.

- High-income professionals and business owners with long accumulation periods.

It does not change concessional contribution caps or standard 15% tax treatment for most Australians.

However, those approaching the threshold may need to consider:

- Contribution timing strategies

- Asset allocation inside super

- Liquidity planning for potential tax liabilities

- Estate planning implications

A proactive discussion with a qualified Box Hill accountant can clarify modelling assumptions and help avoid unintended cash-flow strain.

Why It Matters Now

The debate around Division 296 sits within a broader conversation about superannuation sustainability and fiscal repair. Treasury has consistently framed the reform as targeted rather than systemic, but the political and policy environment remains dynamic.

For high-balance members, waiting until implementation details are finalised may limit planning flexibility.

At Infinity Solution Tax Plus, a trusted accountant in Box Hill can assist with reviewing super structures, stress-testing liquidity scenarios, and aligning retirement strategy with evolving tax settings.

Final Thoughts

Division 296 represents a structural shift in how very large super balances are taxed. While it affects a small proportion of Australians directly, its design — particularly the treatment of unrealised gains — has broader implications for SMSFs and long-term retirement planning.

As legislation progresses, clarity around thresholds, timing, and administration will be critical. Early review, informed modellin,g and measured strategy adjustments remain the prudent course.

Disclaimer: This article contains general information only and does not constitute financial or taxation advice. You should seek personalised advice from a registered tax or financial professional.