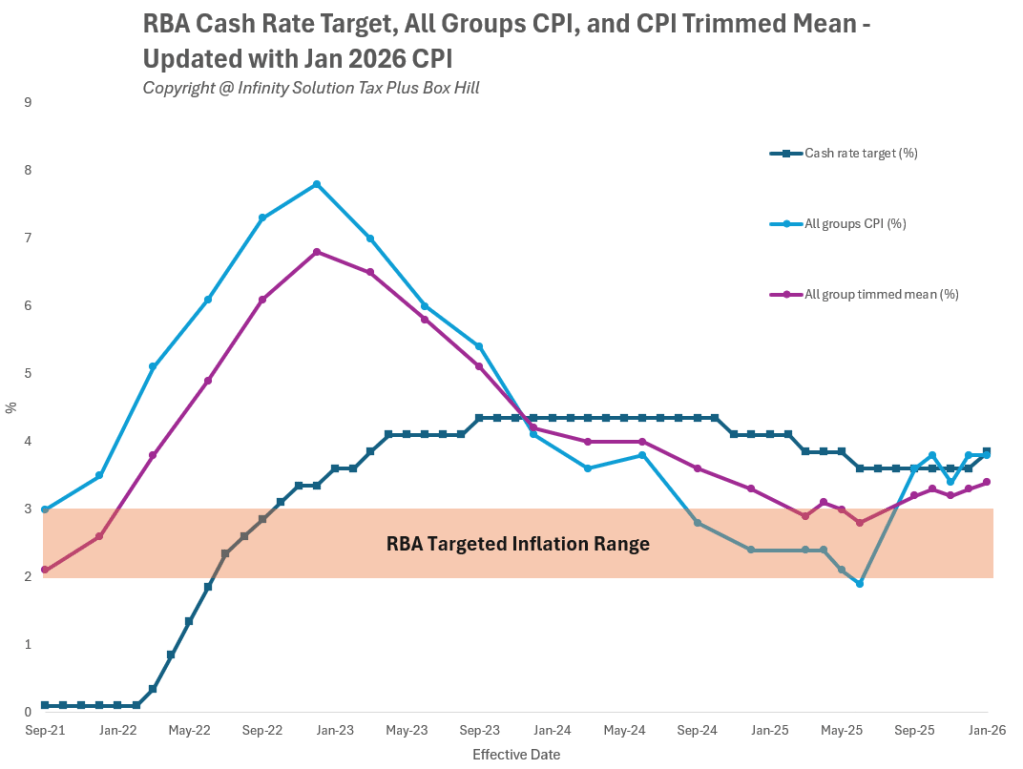

The Reserve Bank of Australia’s February 2026 decision to lift the cash rate target to 3.85% has tangible implications not just for borrowers, but also for savers. The higher policy rates are likely flowing through to savings accounts and term deposits—though unevenly and often with conditions attached. For households reviewing their options with an accountant Box Hill, the key question is how to make savings work harder without taking on unnecessary risk.

The RBA confirmed the rate increase on 3 February 2026, citing inflation pressures that remain inconsistent with its medium-term target and the need to keep policy restrictive for long enough to restore price stability.

Live coverage and commentary over the past week have reinforced how closely interest rates are now tied to everyday cost-of-living decisions, including how households manage cash reserves.

Why Higher Cash Rates Don’t Automatically Mean Better Returns

While the cash rate sets the benchmark, banks adjust savings and term deposit rates based on competition, funding needs, and customer behaviour—not on a one-for-one basis. The RBA’s Statement on Monetary Policy explains that funding costs and competitive pressures vary across institutions, which is why advertised deposit rates can lag, cap out, or rely on “bonus” conditions.

This means savers need to be more deliberate than simply waiting for rates to rise.

Savings Accounts: What to Check Right Now

For at-call savings accounts, headline rates often hide important fine print. Practical checks include:

- Bonus rate conditions – minimum monthly deposits, balance caps, or no-withdrawal rules.

- Reversion rates – what happens if you miss a condition for one month?

- Effective rate after tax – interest is taxable income, which can materially reduce the net return.

In a higher-rate environment, even small differences in conditions can outweigh headline percentage gaps, particularly for households juggling multiple accounts. This is where guidance from a Box Hill accountant can help align savings choices with overall cash flow and tax planning.

Term Deposits: Timing and Flexibility Matter

Term deposit rates have lifted alongside the cash rate, but savers face a trade-off between locking in certainty and retaining flexibility. The RBA has emphasised that future decisions will remain data-dependent, meaning rates could stay elevated—or move again—depending on inflation and labour-market outcomes.

Practical considerations include:

- Staggering maturities rather than locking all funds into one long-term.

- Comparing short-term vs longer-term premiums to see if extra yield compensates for reduced flexibility.

- Understanding break costs, which can be significant if funds are needed early.

Upcoming RBA meeting dates are also relevant for timing rollovers, particularly for shorter-term deposits.

Who Benefits—and Who Needs to Be Cautious

Households with emergency buffers, upcoming large expenses, or uncertain income generally benefit from liquidity, even if that means accepting a slightly lower rate. Those with surplus cash beyond near-term needs may be better placed to lock in higher term rates, provided they understand the tax and access implications.

Final Thoughts

Higher interest rates have restored relevance to cash, but they’ve also made decision-making more nuanced. Savers should focus on net returns, conditions, and flexibility, not just headline rates. With policy expected to remain restrictive for some time, early and informed planning is essential. If you’d like help reviewing savings strategies as part of your broader financial picture, Infinity Solution Tax Plus can assist as your trusted accountant in Box Hill.

Disclaimer: This article contains general information only and does not constitute financial or taxation advice. You should seek personalised advice from a registered tax or financial professional.