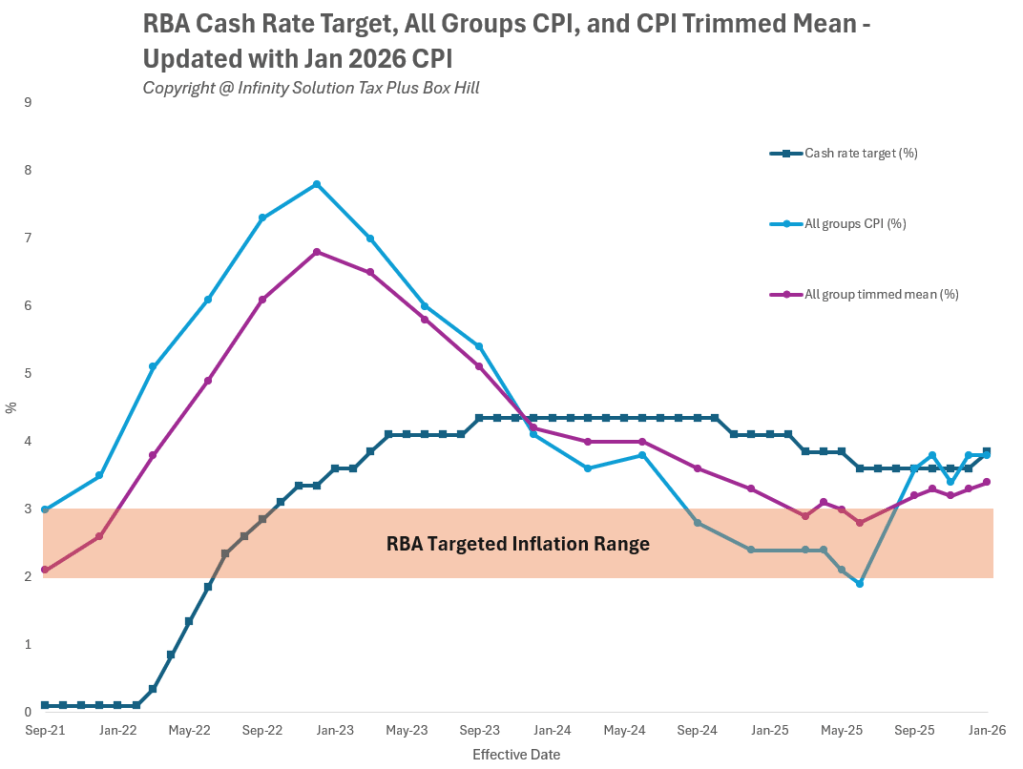

Australia’s cash rate has now risen to 3.85%, marking another tightening step by the Reserve Bank of Australia (RBA) as it continues to press against persistent inflation pressures. For households with a mortgage, this shift is not theoretical—it directly affects monthly repayments, borrowing capacity, and broader household cash flow. For many clients speaking with an accountant Box Hill, the immediate question is what practical steps matter most right now.

The RBA confirmed the decision at its February 2026 meeting, citing slower but still elevated inflation and a labour market that remains tighter than expected. The Bank reiterated that policy needs to remain restrictive for long enough to ensure inflation returns sustainably to the target. Live political and economic coverage over the past week has also reinforced how closely interest rates are now tied to cost-of-living pressures across households.

Why the RBA Lifted Rates

In its February statement, the RBA noted that inflation is likely to remain above target for some time, with capacity pressures and stronger-than-expected private demand. It also noted the labour market remains “a little tight”, and it will be guided by incoming data when deciding what comes next.

The RBA’s accompanying economic outlook (Statement on Monetary Policy – “In Brief”) provides the macro backdrop behind lending and pricing decisions: inflation dynamics, household spending trends, and the balance between demand and the economy’s supply capacity. This context matters because banks often reprice mortgages and serviceability assumptions based on how long restrictive policies might persist.

A Practical Checklist for Mortgage Holders

1) Confirm what you’re actually paying (and when it changes)

Don’t assume the cash-rate move equals the exact change to your home-loan rate or repayment date. Check your lender’s rate-change notice, your direct debit timing, and whether you’re on a packaged or discounted variable rate.

2) Stress-test your repayment buffer

Run a simple “what if” scenario: what happens to your budget if rates rise another 0.25%–0.50%, or if a major expense hits at the same time? The goal is not to predict the next decision — it’s to make sure your cash flow can absorb shocks.

3) Reassess fixed vs variable exposure

If you’re on variable, compare refinance and retention offers (including fees). If you’re rolling off a fixed rate, map the new repayment and decide whether partial refixing provides stability — while keeping some flexibility if rates later ease.

4) Use offsets and redraw strategically

An offset account can be a powerful risk-management tool in a high-rate environment: every dollar in offset reduces interest charged, often delivering a better effective return than many low-risk alternatives after tax.

5) Tighten the “leak points” before you cut the essentials

Before reducing insurance or skipping maintenance, look at discretionary spending, subscriptions, and high-interest consumer debt. The objective is to preserve resilience and avoid expensive short-term fixes later.

Implications and Who Benefits

Borrowers with large loans relative to income, minimal savings buffers, and upcoming fixed-rate expiries are typically the most exposed to repayment shocks. Conversely, households that have built buffers in offsets and maintain conservative spending habits are best placed to ride out a prolonged period of restrictive policy. This is also where a Box Hill accountant can help align mortgage decisions with broader tax-time and cash-flow planning (for example, timing lump sums, managing withholding, and keeping sufficient liquidity).

Final Thoughts

The RBA has been clear that it will remain attentive to the data and evolving risks, rather than committing to a preset path. Mortgage holders should focus on controllables: repayment buffers, loan structure, offsets, and a realistic household budget that assumes rates may stay higher for longer. If you’d like help modelling scenarios and keeping your broader financial position tidy while rates are elevated, Infinity Solution Tax Plus can assist as your trusted accountant in Box Hill.

Disclaimer: This article contains general information only and does not constitute financial or taxation advice. You should seek personalised advice from a registered tax or financial professional.