From 1 January 2026, a significant update to Victoria’s Vacant Residential Land Tax (VRLT) has come into effect. This change expands the tax to include undeveloped residential land that has remained vacant for five or more years, marking an important shift in the state’s property taxation framework.

For property owners, understanding this rule and its exceptions will be crucial to avoiding unexpected liabilities. If you’re uncertain about your exposure to this policy, now is the time to consult a trusted accountant Box Hill for tailored tax advice.

What’s Changing with the Vacant Residential Land Tax?

Previously, VRLT applied mainly to vacant residential properties in Victoria.

From 1 January 2026, the scope of the tax widens to cover any undeveloped residential land that has remained vacant for a continuous period of 5 years or more.

This means landowners holding onto empty residential blocks for long periods could now face an annual VRLT charge, calculated as one percentage (1%) of the site’s capital improved value (CIV).

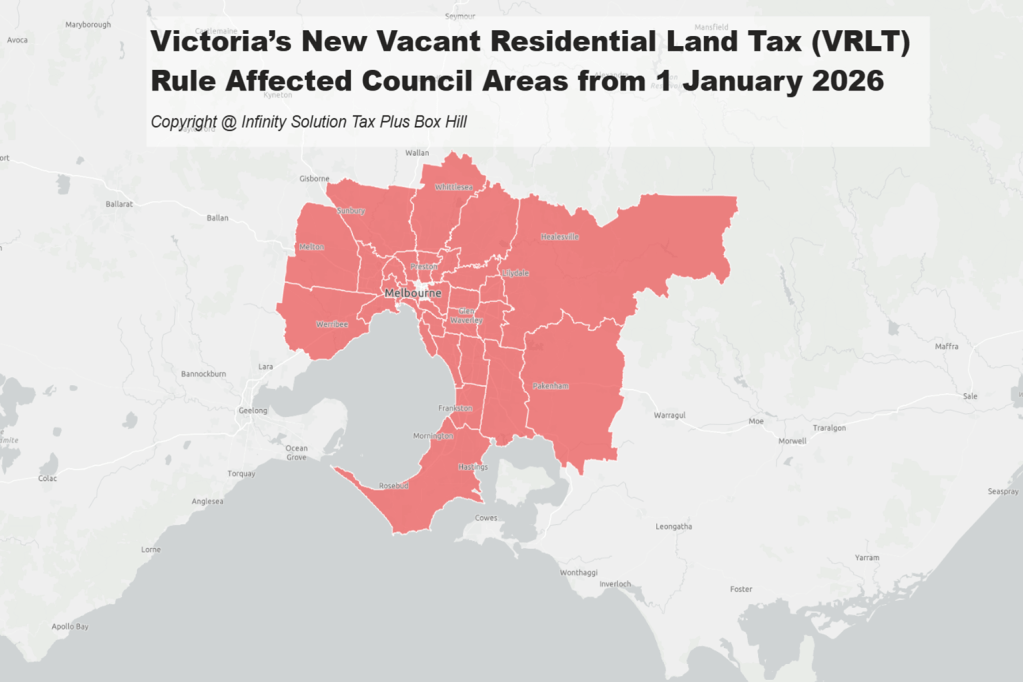

Council Areas Affected by the New VRLT Rules

The extended Vacant Residential Land Tax will apply to land located in the following Victorian council areas:

| Council Area |

| Banyule |

| Bayside |

| Boroondara |

| Brimbank |

| Cardinia |

| Casey |

| Greater Dandenong |

| Darebin |

| Frankston |

| Glen Eira |

| Hobsons Bay |

| Hume |

| Kingston |

| Knox |

| Manningham |

| Maribyrnong |

| Maroondah |

| Melbourne |

| Melton |

| Merri-bek (formally Moreland) |

| Monash |

| Moonee Valley |

| Mornington Peninsula |

| Nillumbik |

| Port Phillip |

| Stonnington |

| Whitehorse |

| Whittlesea |

| Wyndham |

| Yarra and Yarra Ranges |

If your property falls under one of these council jurisdictions, you should review your land’s usage and development timeline carefully.

Does the New Rule Apply Retrospectively?

Yes, the five-year vacancy period is retrospective, meaning that the time your land has already remained vacant prior to 2026 may count toward the five-year threshold.

For instance, if your land has been vacant since 30 Dec 2020, it could be subject to VRLT from 2026 onwards.

This retrospective element is crucial for property investors, developers, and long-term landholders to consider when planning future development timelines or potential sales.

Are There Any Exceptions?

Yes, several exemptions may apply under the VRLT framework, including:

- Primary place of residence: If the land is your main home, VRLT does not apply.

- Land adjoining your PPR: land owned by you and used solely for enhancing your PPR privately may be excepted.

- Land incapable of residential development: the SRO will consider your land’s circumstances to decide whether it should be exempt.

If you think your land should be exempt, you need to make a notification to the SRO before you can apply for an exemption. SRO will contact you regarding the outcome of your application.

How to Prepare for the 2026 VRLT Changes

To avoid potential tax liabilities, landowners should:

- Review property portfolios to identify undeveloped land.

- Confirm the council area your property is located in.

- Keep records showing attempts to develop or use the land.

- Seek expert guidance from SRO to understand your VRLT exposure.

At Infinity Solution, our experienced Box Hill accountants help clients navigate property taxation changes confidently, ensuring compliance while minimising unnecessary costs.

Stay Ahead of Victoria’s New VRLT Rules

With the new VRLT rules taking effect in 2026, it’s vital to act early. Property owners with undeveloped residential land should review their holdings, confirm potential liabilities, and plan development strategies accordingly.

Partnering with a trusted accounting firm like Infinity Solution ensures you stay compliant, optimise your tax position, and protect your investment — all with guidance from a professional accountant in Box Hill.

Contact us on (03) 7046 2254 today to discuss your business case.

Disclaimer: The information contained in this article is general in nature and does not constitute financial or taxation advice. You should seek advice tailored to your specific circumstances from a registered tax or financial adviser.